How does your backlog look?

NFPA’s latest State of the Fluid Power (SOFP) industry survey revealed 49.2% of participating manufacturers reporting a decrease in backlog from May to June 2024.

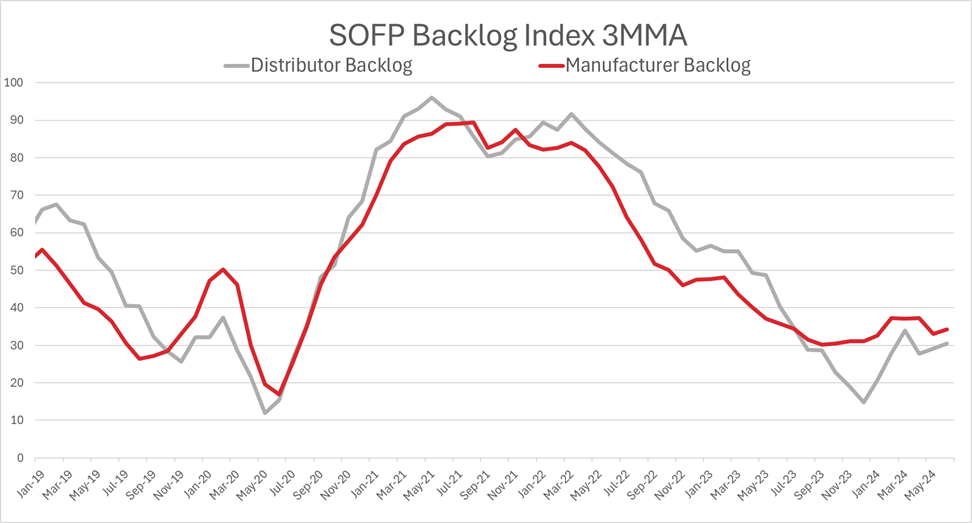

As seen in the graph below, manufacturers and distributors have been saying relatively the same thing about their backlogs increasing or decreasing (higher index = increasing backlog, lower index = decreasing backlog, 50 = same backlog). Backlog levels can be seen increasing rapidly and remaining high during the supply chain issues faced throughout 2021 and most of 2022. Following the supply chain crisis, backlogs have steadily declined throughout 2023 and into Q1 2024. However, the surveys suggest some stabilization over the last couple months.

Why is the backlog so low?

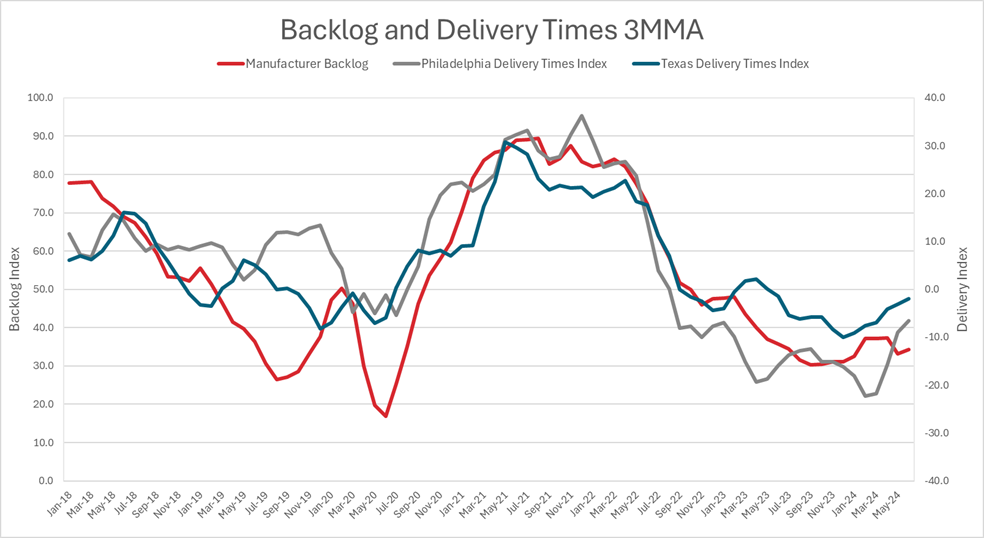

We can look at a few indexes from the Federal Reserve Banks of Texas and Philadelphia regarding manufacturing delivery times. These indexes come from regional manufacturing outlook surveys used to indicate direction of change in overall business activities. The delivery time indexes are calculated by taking the percent reporting increases and subtracting the percent reporting decreases.

Both delivery time indices are over 75% correlated with NFPA’s SOFP Manufacturer’s backlog index. Therefore, historically as backlog levels increased current delivery times also increased and vice versa. Below, you can see how similarly they trend as all three indices are graphed using a 3 month moving average calculation to smooth out their movement. Both began decreasing Q2 2022 until the end of 2023 and beginning of Q2 2024. Philadelphia and Texas's indices have been increasing over the last few months and due to their history of tracking with NFPA's backlog index, this may suggest a turning point for backlog levels as we enter into H2 2024.

When will backlog pressures ease?

The Institute of Supply Management conducts a Supplier Deliveries Index (not shown). This index peaked at 78.8 in May 2021 and troughed at 43.5 in May 2023, both similar to SOFP index’s peak and trough above. Other economic sources are pointing towards a turning point for inventories as we head into the second half of 2024. In the latest World Economic Prospects Report, Oxford Economics states “Though GDP is on track to rise less than we had estimated in Q2, strong household balance sheets, an upswing in equipment spending cycle, a turn in the inventory cycle, and moderating inflation all should support the economy in H2 2024 and early next year.”

If you are interested in participating in NFPA’s State of the Fluid Power Industry Survey, and receiving the finalized report monthly, please contact Cecilia Bart at cbart@nfpa.com or (414) 259-2027.

Like this post? Share it!

Recent Posts

Upcoming Events of 2025!

Trying to plan ahead for future travel? Use this article to lock-in these events into your calendar! Attend a Fluid Power Action Challenge Event and witness hands-on fluid power education! Recruit NIU Engineering Students – Join Us for a Networking Event February 10, 2025 Rockford, IL Economic Update Event: Regional Demand Estimates Report…

Speak with University Fluid Power Clubs this Spring

NFPA Speaker’s Bureau enables industry professionals to present to students enrolled in high schools, tech schools and universities across the country to inspire and excite them about career opportunities in the fluid power industry. We’ve heard from students and instructors that facility tours and campus visits are some of the most effective ways for students…

NFPA Welcomes New Member: GRH America

GRH America headquarter is located in Dallas, Texas, it manufactories hydraulic gear motor, gear pump, orbital motor, valves, HPU in China. GRH America sells OEM companies and works with distributors to sell its products. GRH America20181 S. Highway 78Leonard, TX 75452469-399-5700www.grhamerica.com OCR: Dick Cai, President & CEOdcai@grhamerica.com